SB 253 Compliance,

Made Manageable!

California’s Climate Corporate Data Accountability Act (SB 253) is now in force, with the first reporting deadline set for August 10, 2026. If your company does business in California and exceeds $1 billion in annual revenue, the clock is already running. Net0Trace gives you an audit-ready path from raw activity data to compliant emissions disclosure — built on the GHG Protocol, automated with AI, and designed to scale as the rules tighten through 2027 and beyond.

Who Must

Comply with

SB 253?

SB 253 applies to U.S. companies with total annual revenue greater than $1 billion that “do business in California.” SB 253 requires

these companies to disclose their Scope 1, 2, and 3 emissions and to obtain independent third-party assurance of that data.

The threshold is based on the gross receipts definition in California's tax code, and applicability is determined by the lesser of your two previous fiscal years of revenue — counting total gross receipts regardless of whether that revenue was generated inside California.

A company is considered to be doing business in California if it is actively engaging in a transaction for financial gain, and during any part of the reporting year it is either organized or commercially domiciled in California, or its California sales exceed the inflation-adjusted threshold (set at $735,019 for 2024). Notably, CARB's definition excludes the tax code's references to property holdings and payroll, having determined those alone don't establish a sufficient economic connection to the state.

Tax-exempt nonprofits, government entities (and majority government-owned companies), insurance companies, businesses whose only California activity is payroll or remote-worker compensation, and businesses whose only California activity is wholesale electricity transactions are exempt.

Deadlines

August 10, 2026 — Scope 1 & 2 reporting. companies report Scope 1 and 2 GHG data, and no assurance is required for this first submission. The reporting period depends on your fiscal year end: companies whose fiscal year ends between January 1 and February 1, 2026 report data from the fiscal year ending in 2026; those whose fiscal year ends between February 2 and December 31, 2026 report data from the fiscal year ending in 2025.

2027 — Scope 3 added, plus assurance begins. Scope 3 emissions reporting is required starting in 2027, and limited assurance on Scope 1 and 2 emissions also begins that year. CARB is still finalizing the Scope 3 phase-in approach, weighing options including broad applicability, a sectoral phase-in, and a category-by-category phase-in.

2030 and beyond. Reasonable assurance of Scope 1 and 2 data and limited assurance of Scope 3 data are scheduled to begin in 2030 (covering 2029 data).

The “Good Faith” Window Is Not a Reason to Wait

CARB is exercising enforcement discretion for the first year, stating it will not impose penalties on companies acting in good faith during the first reporting cycle. CARB has said it will not take enforcement action against incomplete Scope 1 and 2 reporting in year one as long as companies make a “good faith effort” to comply.

Here’s the catch: good faith requires demonstrable effort. Enforcement discretion is not a holiday — it’s a grace period for companies that can show they are actively building toward compliance. A company with no data, no process, and no documented attempt has nothing to demonstrate. Starting now is the safest path: it converts the grace period from a risk into a head start, and it positions you for the 2027 assurance requirements that arrive with no such leniency.

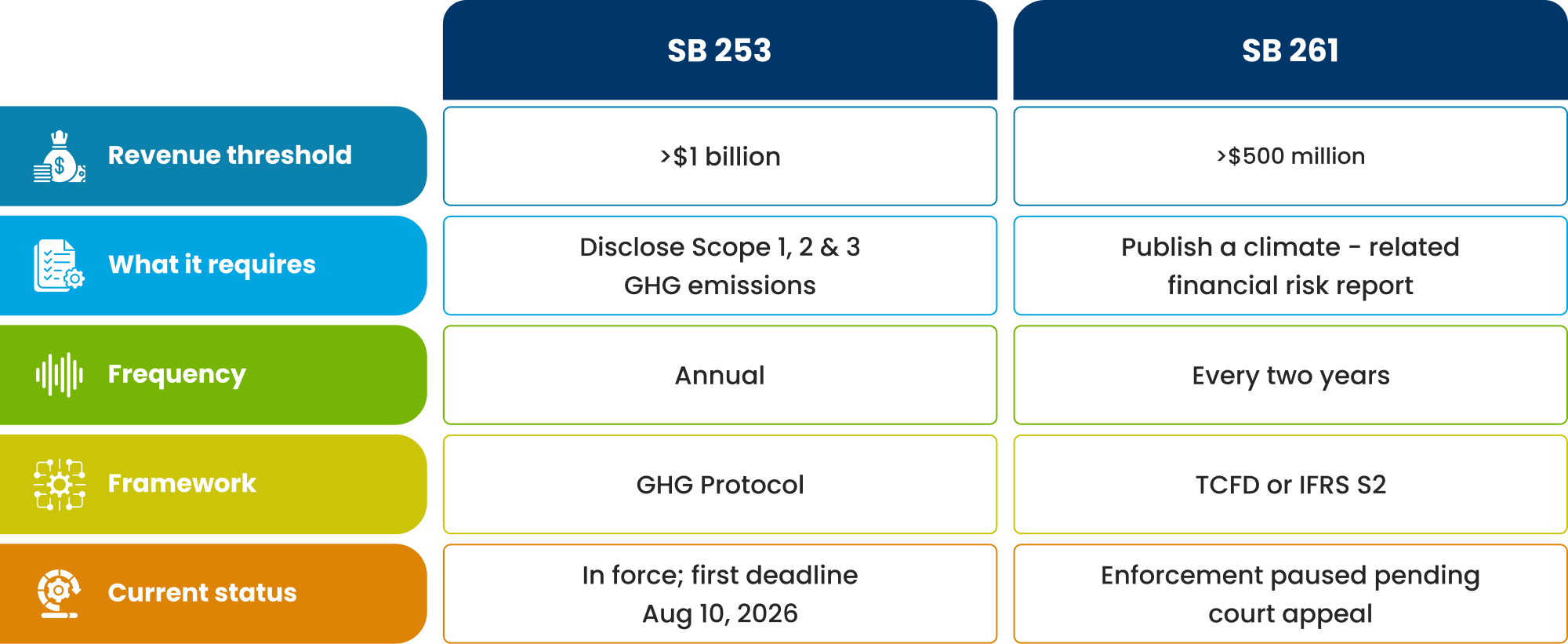

SB 253 vs. SB 261 —

Know Both Thresholds?

Many companies caught by SB 253 are also caught by its sister law, SB 261 — and the two are frequently searched and confused together.

How

Net0Trace Works

the GHG Protocol for emissions calculations — and Net0Trace is built on that foundation from the ground up.

Connect your operational, energy, procurement, and travel data from across the organization. Net0Trace centralizes fragmented inputs — utility bills, fuel logs, ERP records, supplier data — into a single structured emissions ledger, eliminating the spreadsheet sprawl that derails first-time reporters.

Net0Trace automatically matches your activity data to the correct emissions factors, drawing on recognized public datasets. CARB has pointed to sources including EPA's eGRID, the EPA Emission Factors Hub, the IPCC Emission Factor Database, and the USEEIO input-output model. Our AI handles the mapping at scale, so you're not manually reconciling thousands of line items.

Every calculation follows GHG Protocol methodology, with support for the organizational boundary approaches CARB is standardizing. CARB has proposed both an equity-share approach and a control approach (financial or operational) for setting boundaries — Net0Trace accommodates either.

Every figure is traceable back to its source input, with a complete, timestamped record of methods, factors, and assumptions. This is exactly the documentation that demonstrates the "good faith effort" CARB expects in year one — and the evidentiary backbone assurers will demand in year two.

No assurance is required for the 2026 reports, but limited assurance on Scope 1 and 2 data becomes mandatory in 2027. CARB has proposed a set of recognized assurance standards including ISSA 5000, ISAE 3000/3410, AICPA AT-C sections, AA1000AS, and ISO 14064-3. Net0Trace structures your data to those standards now, so when assurance becomes mandatory you're not rebuilding — you're ready.

The companies that treat the first year as a dry run — not a pass — will be the ones who breeze through assurance.

Why Choose

AIROI?

larger sustainability story. AI ROI built Net0Trace as part of a connected carbon and ESG ecosystem, not as a standalone calculator.

The same emissions data that satisfies SB 253 feeds directly into:

Carbon credit strategy

Once you can measure precisely, you can identify reduction opportunities and manage offset and credit decisions with real numbers instead of estimates.

Broader ESG and disclosure reporting

Operational decision-making

Revenue Threshold

What it requires

Publish a climate-related financial risk report